Advantages of Bridging Finance UK

- Bridging Loans can be obtained speedily and borrowers can often get an instant approval

- There are rarely credit checks and personal income is not used to decide the eligibility

- There is flexibility in both the way the loan is paid back and the way the interest is paid back

Disadvantages of Bridging Finance Solutions

- Interest rates are higher

- There are lots of fees to consider

- Assets are at risk if repayments cannot be made.

What are first and second charge Bridging Loans?

Basically a first charge is a primary mortgage or loan secured against a property by the lender. Most lending is on a first charge basis and a second charge can only be secured if there is sufficient equity in the property. The first charge lender has to agree to a second charge loan being taken out. Interest rates tend to be higher on second charge loans because the risks are higher for the lender.

What Are Open and Closed Bridging Finance Solutions?

A borrower taking out an open bridging loan will not have an exit strategy in place, or their exit strategy will have no fixed end date.

The risks are higher, and as you might expect, the rates are higher. Open loans are often declined because the lender will need to know how the borrower will return the finance.

One example of an open loan could be equity tied up in a property, which is not yet on the market.

To secure a closed loan there must be a clear exit strategy planned out so the lender will have a clear idea of when and how the loan will get repaid. It’s in the investor’s interest to have a well thought out exit strategy as the penalties for getting it wrong can be high. Some lenders will place borrowers in default if they are unable to pay back loans which will affect credit ratings some may even start the process of repossession and some will allow the loan to extended – but will charge hefty fees for the privilege.

What Are the Eligibility Criteria for Bridging Loan Finance?

Typically bridging lender can lend 75% gross loan to value, what this means is they will lend 75% included the interest rolled up, in some instances if you can demonstrate serviceability of the loan then you can get 75% net loan to value. We use a 75% LTV as the default on our bridging finance calculator.

|

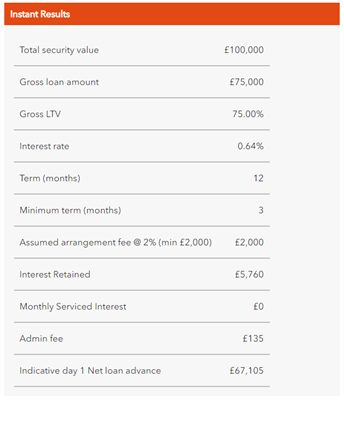

Interest Deducted Bridging Finance

|

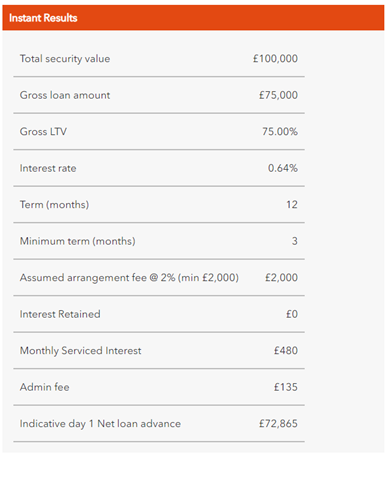

Interest Serviced Bridging Loan

|

|

|

Use our residential and commercial briding finance calculator for your bridging finance needs.

How Much Does Bridging Finance UK Cost?

Fees will vary from lender to lender but commonly incurred costs include broker fees a valuation fee legal costs and arrangement fees, also known as facility fees. There is also the exit fee to consider. If the loan amount required isn’t that much and the project is less risky, the lender is likely to offer better rates and fees. But if the project needs lots of money fast fees can be higher. All fees aside from exit fees are usually deducted before the loan amount is paid.

There will also be solicitor’s fees for both the lender and the borrower. The lender’s solicitor will double-check all the information sent over by the borrower’s solicitor and approve the loan once they are satisfied.

Interest can be paid back in a variety of ways. It can be paid at the beginning along with the fees or it can be paid in one lump sum at the end, often popular with borrowers without a regular cash flow. Retained interest is a mix between the two. These are monthly repayments negotiable depending on the terms of the loan.

How Long Does a Bridging Loan Financing Application Take?

As well as factoring in the speed at which it takes the lender's solicitor to double-check everything, it will depend on other factors such as:

- The time it takes for the valuation to come back.

- Whether a primary lender needs to approve a second charge loan.

- How long that takes and depending on the lender how much information they need on the borrower themselves.

Although time frames vary, the process should take no longer than a month; bridging loans are designed to be speedy, and a bridging finance calculator provides immediate indicative calculations.

How Much Can You Borrow From Bridging Finance Companies for a Buy to Let Investment?

Unlike a mortgage, your income and rental income don’t factor into it. The bridging loan is calculated on the property value alone, but different lenders work out values in different ways – a bridging finance calculator bases estimates on averages.

Try out our Bridging Finance Loan Calculator

Whereas a mortgage value will be based on the lower of the current property value or buying price, some bridging lenders use the market value when consulting their own bridging finance calculator.

And some lenders will also calculate loans based on what they estimate the property will sell for after development - this is known as the Gross Development Value (GDV).

In this case, they will provide an initial loan based on the purchase price (i.e. before refurbishment) and offer a second stage of the loan once the property has been refurbished and its value increased.

Investors who want to borrow more money for big restoration projects will need to consider how lenders calculate valuations.

Why is a Valuation So Crucial to Bridging Finance Companies?

Lenders can take legal action over money lost due to an inaccurate valuation, so they will have the property independently valued by an RICS surveyor rather than using a standard bridging finance calculator.

Lenders will also want to ascertain a few things before agreeing to a loan.

They might ask questions about the experience as a property investor, how the borrower will pay the loan back, what other assets are owned and any income the investor receives.

Taking out a bridging loan can be a fruitful investment if everything is considered before and the pros and cons are weighed up, beginning with a bridging finance calculator to estimate the total costs.

The borrower needs to be honest about when and how they will repay the loan to prevent penalties.

Having a clear exit strategy with contingency plans will prevent grief later down the line.

By calculating fees and interest with different bridging lenders, borrowers can have a rough idea of costs, which should help weigh up whether the investment will be worth it – a bridging finance calculator is a quick and free solution to get you started.

The right solicitor can ensure the transaction runs smoothly. Some solicitors specialise in bridging loans to finance buy to lets and are accustomed to the legalities surrounding them.

Benefits of Working With a Bridging Finance Expert

A bridging loan expert will be able to tell within a few days whether they think a loan will be accepted and will offer advice on how to proceed.

As with all big financial decisions, it's best to be armed with the knowledge to make the right decision in the first place.

Why not try out our Bridging Loan Calculator to see how much you could borrow.